Derivative. Sounds silly, right? It sounds like the noise made when someone drinks water too fast and it goes down the wrong pipe. Fancy television food critics might say it when describing a chef’s deconstructed meatloaf.

Derivative. Sounds silly, right? It sounds like the noise made when someone drinks water too fast and it goes down the wrong pipe. Fancy television food critics might say it when describing a chef’s deconstructed meatloaf.

In finance, derivative is a common term. It’s a financial instrument used globally by organizations of all kinds – from non-profits and hospitals to multi-national corporations. Derivatives are most often used by entities to hedge their currency, commodity or interest rate risk. They are also a relatively inexpensive vehicle used to speculate, and earn a return over and above what traditional investment instruments may yield.

So, what is it? While authoritative bodies and standard setters have varying definitions [1], a derivative is widely known as a contract between two or more parties whose value is derived from an agreed-upon underlying financial asset, index, or security. Common underlying instruments include bonds, commodities, currencies, market indexes, and stocks.

Derivatives are either traded through an exchange or central clearing house, or they are traded over-the-counter (“OTC”) using a swap dealer or counterparty broker. Exchange-traded or “cleared” derivatives are standardized contracts, possessing like terms and attributes that allow it to be traded freely and frequently by industry participants. OTC contracts, on the other hand, are highly tailored contracts that users may customize for their own needs and objectives.

A derivative is expected to generate future cash flows. Thus, it has a value. This value changes every day. It may be positive (an asset to the user) or negative (a liability to the user), and it should be recorded and disclosed in an entity’s financial statements. Variability inherent in derivative valuation gives rise to a zero-sum game wherein the value is an asset to one party and a liability to the other, and vice-versa. Thus, the owing party is expected to provide some consideration to reduce the credit risk assumed by the other. As such, derivatives often involve collateral. That is, users are responsible for pledging (or receiving) collateral in the form of cash or highly-liquid treasury securities to a margin account. The margin account serves to reduce credit risk and to offset the receiving party’s exposure.

A derivative is expected to generate future cash flows. Thus, it has a value. This value changes every day. It may be positive (an asset to the user) or negative (a liability to the user), and it should be recorded and disclosed in an entity’s financial statements. Variability inherent in derivative valuation gives rise to a zero-sum game wherein the value is an asset to one party and a liability to the other, and vice-versa. Thus, the owing party is expected to provide some consideration to reduce the credit risk assumed by the other. As such, derivatives often involve collateral. That is, users are responsible for pledging (or receiving) collateral in the form of cash or highly-liquid treasury securities to a margin account. The margin account serves to reduce credit risk and to offset the receiving party’s exposure.

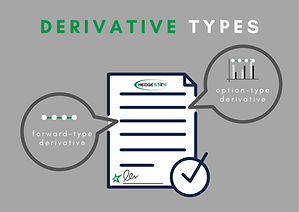

There are many different flavors of derivatives and the volume of variations is only expected to increase – a prophecy fulfilled almost entirely by the OTC markets. We can distill most derivative types into two groups: forward-type and option-type. Users of forward-type derivatives can set a rate or price today that obligates them to take delivery or settlement of an asset for that rate or price in the future. Common examples of forward-type contracts are futures and swaps. Users of option-type derivatives set a rate or price today that gives them the right, but not the obligation, to take delivery or settlement of an asset for that rate or price in the future. Option-type contracts may cause the user to pay or receive a premium upfront, which is common for net purchase or sell options, respectively. Option-type contracts allow users to reduce the risk of rate or price changes above or below certain levels. For example, a purchased call option compensates the option holder for price changes above the strike price (but not below). Option-type contracts bear similar resemblance to traditional insurance. Common examples include calls, puts, and collars. There are bespoke derivatives that possess some combination of both forward-type and option-type characteristics, but those are better left discussed at another time and place.

Derivatives are an ever-evolving byproduct of a capital markets system that is changing constantly to meet participants’ needs. That said, when you dive into the details and understand the drivers of value, you’ll find that derivatives are not as complicated as they seem. Derivatives are more akin to learning a new language rather than learning how to do a double backflip. So, if you’re a multilingual gymnast, derivatives are easy! If you’re not, let HedgeStar be your ‘rosetta stone’ and guide you toward derivative enlightenment.

Derivatives are an ever-evolving byproduct of a capital markets system that is changing constantly to meet participants’ needs. That said, when you dive into the details and understand the drivers of value, you’ll find that derivatives are not as complicated as they seem. Derivatives are more akin to learning a new language rather than learning how to do a double backflip. So, if you’re a multilingual gymnast, derivatives are easy! If you’re not, let HedgeStar be your ‘rosetta stone’ and guide you toward derivative enlightenment.

[1] For example, the Commodity Futures Trading Commission expands its definition to state that derivatives are “used to hedge risk or to exchange a floating rate of return for a fixed rate of return.” The Financial Accounting Standards Board dedicated approximately 56 paragraphs to describe the myriad traits of a derivative at Accounting Standards Codification topics 815-10-15-83 through 15-139.